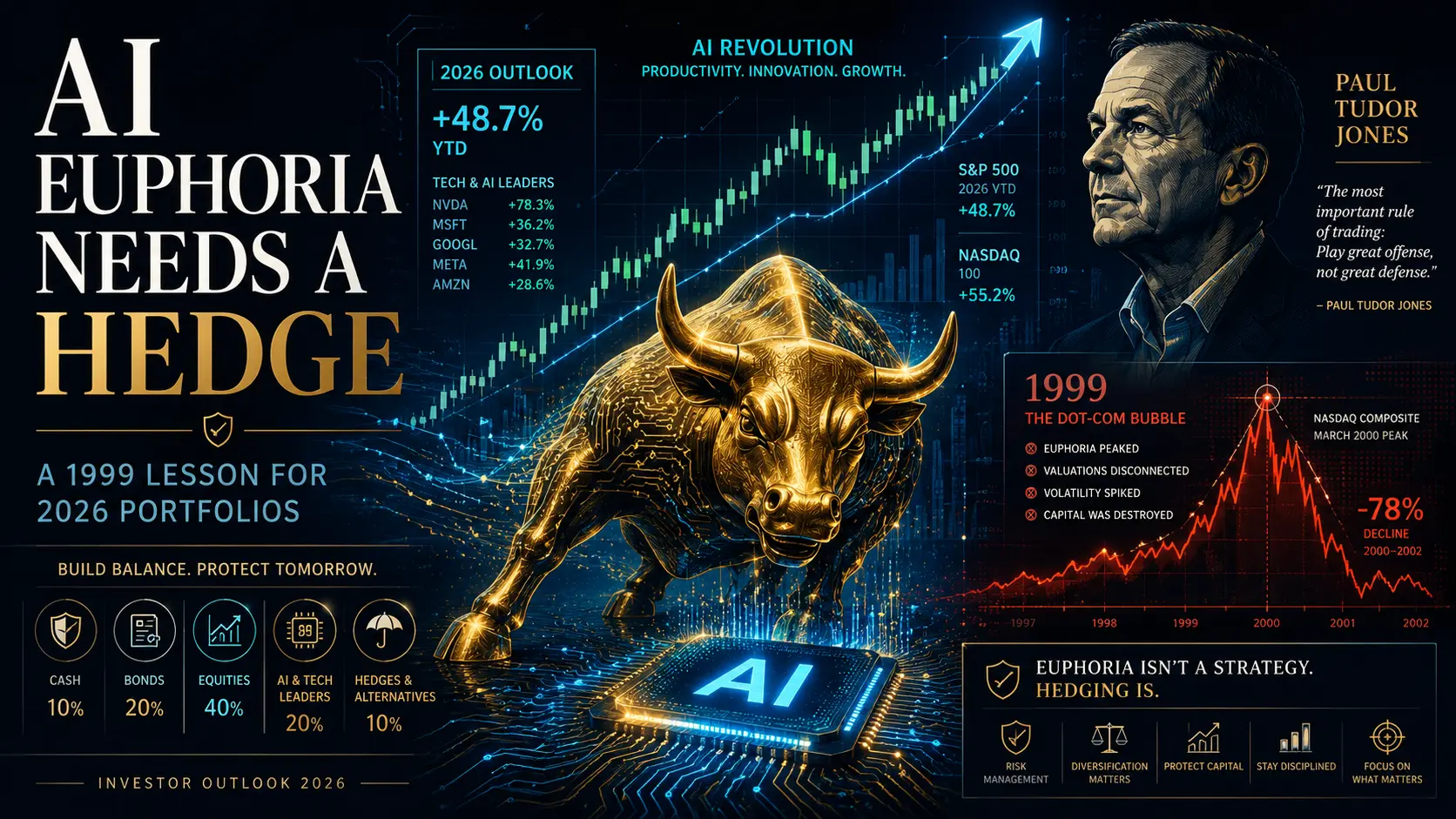

On May 7, 2026, billionaire hedge fund manager Paul Tudor Jones told CNBC's "Squawk Box" something that should make every investor pause: the artificial intelligence bull market still has another year or two of upside, but when it ends, the correction could be "breathtaking." He compared the current moment to October or November of 1999, roughly four months before the dotcom bubble peaked in March 2000. That comparison is not a casual remark from a market commentator. It is a calibrated warning from one of the most respected macro traders alive, and it arrives at a moment when the S&P 500 keeps printing records, the Nikkei 225 has just crossed 62,000 for the first time in history, and gold is trading above $4,700 per ounce as a hedge against the very turbulence Jones describes.

If you are an investor in 2026, you are facing a paradox that Jones himself embodies. He is bullish enough to be adding AI exposure to his own book. He is bearish enough to warn that the eventual unwind could resemble the worst tech crash in modern memory. How do you act on a thesis that says "ride the rally, but know the exit will be ugly"? That is exactly what this article unpacks. We will explore what Jones actually said, why the 1999 parallel cuts both ways, the four critical differences that make this cycle structurally different, and the concrete portfolio moves prudent investors are making right now to capture upside without being wiped out when the music stops.

The remarks that lit up financial media did not come from a permabear or a contrarian newsletter writer. Paul Tudor Jones is the founder and chief investment officer of Tudor Investment Corporation, a macro hedge fund firm that has navigated four decades of market cycles, including a famous call ahead of the 1987 crash. When a trader of that caliber draws a specific historical analogy on national television, professional risk managers listen.

Jones framed his thesis around two technological inflection points. The first comparison was to Microsoft's emergence as a dominant software platform in 1981, the early years of the PC revolution. The second was to the commercialization of the internet in the mid-1990s. He argued that the launch of advanced AI assistants, including Anthropic's Claude in January 2026 and OpenAI's continued evolution of ChatGPT, marks a similar productivity inflection. In his framing, both prior eras delivered roughly four to five and a half years of compounding equity returns once the productivity story took hold.

If that math is right, and if early 2024 marks a reasonable starting point for the current AI investment cycle, then we are roughly halfway through a multi-year bull run. That is the constructive part of the message.

The cautionary part of the message is what makes the comparison sharp. Jones specifically said the current environment, viewed through the lens of valuation multiples and earnings indicators, looks closer to October or November of 1999 than to the early phase of the internet boom. The dotcom market peaked on March 10, 2000. By that calendar, today's investors might be operating in a window where most of the easy gains lie ahead but the late-stage froth, melt-up, and eventual top are also coming into view.

Jones laid out a specific quantitative scenario. If the U.S. stock market climbed another 40% from current levels, the ratio of total stock market capitalization to gross domestic product would reach somewhere between 300% and 350%. That would dwarf the 2000 peak, when the same ratio reached approximately 140%, and it would create the conditions for what Jones called a "breathtaking" correction. Risk managers know that drawdowns from extreme valuation levels tend to be both deeper and longer than declines from normal valuations.

The detail that truly defines Jones's thesis is what he is doing with his own capital. Despite warning of a potentially historic correction, he confirmed that he has recently increased his AI-related positions. As a self-described macro trader, he buys baskets rather than picking individual names, and his stated belief is that he can navigate the eventual exit. This is the calculus of a professional who trusts his own ability to read the cycle and act before retail investors realize the regime has changed.

For most individual investors, replicating that approach without institutional infrastructure is risky. The lesson is not "do exactly what Jones is doing" but rather "respect the thesis and build a portfolio that survives even if you cannot perfectly time the exit." That is where behavioral discipline and proper risk frameworks become decisive.

Pattern recognition is one of the most useful skills in markets, and the surface similarities between today's AI rally and the late 1990s are real. Skeptics are not making them up. Acknowledging the parallels honestly is the first step toward acting on them rationally.

Index concentration in a handful of mega-cap names. In 1999, a small group of technology stocks drove a disproportionate share of the Nasdaq's gains. In 2026, the so-called Magnificent 7 collectively account for an unprecedented share of S&P 500 market capitalization, and the AI infrastructure subset of that group is even more concentrated. When a market relies on a narrow leadership group, it becomes vulnerable to sentiment shifts in just a few names.

Narrative dominance. During the dotcom era, attaching ".com" to a company name was enough to lift its valuation. Today, mentioning AI in a strategy update, a product roadmap, or even a SaaS pitch deck triggers a similar valuation premium. When the descriptive label of a sector starts to function as a magic word that suspends normal scrutiny, that is a textbook late-cycle behavior.

Vendor-financed mega-deals. The 1990s telecom boom saw equipment vendors lend money to customers so those customers could buy more equipment, inflating reported revenues. Today's headlines about multi-billion-dollar partnerships in which chipmakers, hyperscalers, and AI labs cross-invest in each other have raised the same kind of eyebrows from credit analysts. Whether these arrangements are economically sound or accounting theater will determine a lot about what survives a downturn.

Retail euphoria and IPO behavior. The dotcom era was defined by first-day IPO pops of 58% to 73% on average, with most listed companies reporting losses. The 2026 environment has not yet matched those extremes, but private market valuations for AI startups, the velocity of secondary share sales, and the willingness of retail investors to buy single-name AI exposure on margin all rhyme with the speculative tone of late-stage bull markets. Recognizing these signals is one of the most common mistakes in stock market investing that even experienced participants overlook.

Cycles rhyme but they do not repeat exactly, and the case that this AI cycle is structurally healthier than 1999 is not just bullish hand-waving. It rests on four observable differences in earnings, infrastructure, addressable market, and macro backdrop.

Earnings are real and concentrated in profitable platforms. The dotcom poster children were burning cash to fund customer acquisition and hoping that a viable business model would emerge before the runway ran out. The 2026 AI infrastructure leaders, by contrast, are reporting tens of billions of dollars in quarterly revenue, expanding gross margins, and free cash flow that funds continued capital expenditure. The difference between selling shovels in a real gold rush and selling maps to a hypothetical gold field is exactly the difference between most AI infrastructure plays today and most dotcom darlings then.

Capital expenditure is physical and useful. A massive share of AI investment in 2026 is going into data centers, electrical grid upgrades, and chip fabrication facilities. Even in a severe correction scenario, that physical capacity does not evaporate. The dotcom era similarly funded a buildout of fiber optic capacity that, after the crash, became the substrate for the next decade of internet growth. Today's data center boom is following the same pattern, only at a far larger physical and energy scale.

The addressable market is bigger by an order of magnitude. Internet adoption in 1999 was largely about replacing offline information transfer with online equivalents. AI in 2026 is positioned to automate cognitive labor across the entire knowledge economy, which represents a far larger pool of value than software spending alone. Some research has suggested AI's total addressable market could reach roughly 11 times the historic scale of IT spending, because it extends into labor productivity rather than just IT budgets.

The macro backdrop is more nuanced. The Federal Reserve has held its benchmark rate at 3.50%–3.75% through three consecutive 2026 meetings, a level that constrains speculative excess in a way that the much lower rates of the late 1990s did not. At the same time, the prospect of incoming Fed leadership and a midterm election cycle could limit aggressive tightening, creating a cushion that did not exist in earlier corrections. Understanding how interest rates shape investment choices is critical to interpreting how this backdrop will evolve over the next twelve to eighteen months.

Putting concrete figures around the macro thesis turns it from abstract narrative into something investors can stress-test against their own portfolios. Three metrics deserve particular attention right now.

The first is the market capitalization to GDP ratio, often called the "Buffett Indicator" because Warren Buffett once described it as the single best measure of equity valuation. A ratio approaching 200% has historically been associated with rich valuations. The 300%–350% range Jones described would be unprecedented in modern U.S. financial history. Reaching that level would imply either extraordinary earnings growth ahead or a dramatic divergence between asset prices and economic output, the latter being exactly what defines a bubble.

The second is index concentration. When the largest five or ten constituents of an index drive the majority of returns, the index becomes a leveraged bet on those few names rather than a diversified market exposure. Investors who believe they are diversified by holding a broad U.S. equity index in 2026 should look closely at the underlying weightings before assuming their portfolio reflects the economy.

The third is forward earnings yield versus risk-free rates. In 1999, the spread between the S&P 500 earnings yield and 10-year Treasury yields had collapsed to historically low levels, signaling that equities offered little compensation for taking on risk. Tracking that spread in 2026 — and comparing it to the levels that historically preceded major drawdowns — is one of the more reliable warning systems available to long-term investors. Tools like the Sharpe ratio can help quantify whether the return investors are receiving justifies the risk they are taking on at any given valuation level.

Reading Jones's thesis as "the rally is over, sell everything" would be a misreading. Reading it as "buy the dip, AI to the moon" would be equally wrong. The actionable interpretation sits in the middle: stay invested in the productivity revolution, but engineer your portfolio so a 40%–60% drawdown in concentrated AI exposure does not destroy your long-term financial plan.

The single most expensive mistake an investor can make in a late-stage bull market is to sell everything months before the actual peak. The dotcom era produced a long list of investors who exited in 1998, missed the final melt-up, and then watched in frustration as their target prices were left behind. The pain of missing returns is real, and most people who try to come back in do so too late. Jones himself is adding AI exposure precisely because he respects the cost of being out of a parabolic move. The discipline is to participate, not to abstain.

Concentrated AI exposure can coexist with broader diversification. That means meaningful allocations to non-U.S. equities, where valuation multiples remain more reasonable, and to asset classes that historically perform well during equity drawdowns. Gold above $4,700 per ounce is signaling that institutional investors are already taking this seriously. Considering crisis-proof investments and resilient sectors is not bearish positioning — it is portfolio insurance that lets you stay in the AI trade with confidence.

Position sizing is the most underrated discipline in retail investing. If a single AI stock is 30% of your portfolio, a 60% decline in that stock is a 18% drawdown to your total wealth — recoverable but painful. If the same stock is 5% of your portfolio, the same decline is a 3% drawdown, almost invisible against normal market noise. The same upside conviction can be expressed at very different risk levels depending on how the position is sized. Building a coherent risk management framework is what separates investors who survive multi-year regimes from those who do not.

For investors with meaningful AI exposure, hedging instruments such as protective puts, collar strategies, and inverse exposure to concentrated indices can convert tail risk into a known, manageable cost. The economics of hedging are unfavorable in calm markets — premiums look expensive when nothing seems to be happening. The economics of hedging are extraordinary in crisis markets — exactly when investors most regret not having the protection in place. Building familiarity with effective investment hedging strategies before you need them is a hallmark of serious portfolio construction.

The 2000–2002 unwind of the Nasdaq, which saw the index fall by roughly 78% from its peak, generated a number of durable lessons that remain valid in any concentrated bull market.

The first is that survivors and victims often look identical at the peak. Amazon, eBay, Cisco, and many other recognizable winners of the post-crash era saw their stock prices collapse 80% or more during the bear market. The companies survived; many investors holding them at peak valuations did not. Distinguishing between a great business and a great stock at a particular price is the central skill that separates strategic from speculative investors.

The second lesson is that liquidity vanishes when you most need it. During the worst stretches of the dotcom unwind, bid-ask spreads widened, certain securities effectively could not be sold at any reasonable price, and margin calls forced sales at the worst possible moments. Investors who used leverage discovered that their effective risk was much higher than they had modeled. Anyone running margin in 2026 should stress-test their position against a 40% peak-to-trough decline in their largest holdings.

The third is that the next bull market emerged from completely different leadership. The post-2002 recovery was led by financials, energy, materials, and emerging markets, not by the survivors of the prior cycle. Investors who anchored their thesis to "tech will lead again" missed an entire decade of returns elsewhere. The implication for 2026 is to stay open-minded about where the next leadership group emerges, even while continuing to participate in the AI cycle. Identifying undervalued assets outside the consensus theme is exactly the discipline that pays off after major regime changes.

Direct stock picking in AI infrastructure names is not the only way to express a bullish thesis on the cycle, and in many cases it is not the most prudent way. Investors building positions today have several diversified vehicles available that can capture the upside while mitigating single-name risk.

Thematic ETFs covering AI and automation. Diversified AI-focused ETFs provide exposure to the broad supply chain — chip design, foundry capacity, software platforms, data center REITs, electrical infrastructure — without requiring the investor to pick which specific company within each layer will dominate. This is closer to the basket approach Jones himself describes using.

AI-driven portfolio management. A growing share of capital is being managed by autonomous AI trading agents and algorithmic trading strategies that use machine learning to dynamically adjust exposure based on market conditions. The same technology that is fueling the bull market is also being deployed to manage risk within it. For investors comfortable with quantitative approaches, this represents a way to participate in the productivity revolution from both sides — as an investor in AI and as a user of AI-powered allocation.

Tactical algorithmic exposure. Even traditional investors are increasingly augmenting their core holdings with profitable algorithmic trading strategies that systematically harvest factors such as momentum, low volatility, and quality. These factor-based approaches have historically held up better during sharp index drawdowns than passive market-cap-weighted exposure, because their underlying screens tend to rotate away from the most overvalued names automatically.

The common thread across all three approaches is that they replace single-name conviction with system-driven diversification. In a market where the leadership names could fall 60%–80% in a correction, replacing concentration with structure is not bearish — it is strategic.

Late-stage bull markets are not primarily defeated by bad analysis. They are defeated by predictable psychological patterns that distort otherwise capable investors into making decisions they later cannot defend. Understanding these patterns is the closest thing to an investing superpower available to anyone.

Fear of missing out (FOMO) drives investors to chase performance into already-extended stocks, typically at the worst possible entry points. The pain of watching peers profit from a name you avoided is psychologically real, but it is not a basis for an investment thesis. Setting predefined entry rules — and respecting them even when sentiment is screaming louder — is the antidote.

Recency bias convinces investors that the recent past will continue indefinitely. After a year of strong AI returns, the brain extrapolates linearly: "this will keep working." Markets do not work that way. The probability of mean reversion increases with the duration and magnitude of the prior move, not the other way around.

Confirmation bias filters out information that contradicts an existing thesis. Investors who are heavily long AI tend to read more bullish AI commentary, follow more bullish AI commentators, and subconsciously dismiss bearish data points. Actively seeking out the strongest counterargument to your own positioning — and engaging with it seriously — is a discipline that improves outcomes more than any technical indicator.

Anchoring locks investors onto historical purchase prices, leading to decisions like refusing to sell a winner because "it has already gone up so much" or refusing to sell a loser because "it has to come back to my entry." The market does not know what you paid. Decisions should be made based on forward expected returns from current prices, not on the path that brought a position to its current level.

A deeper understanding of how emotions affect investment decisions and how to develop a successful investor mindset is, in many ways, more valuable in 2026 than any specific market call. The investors who navigate the next two years successfully will be the ones who control their behavior, not the ones who predict the exact peak.

The honest answer is that it shares characteristics with historical bubbles — index concentration, narrative dominance, stretched valuations in select names — but it also has characteristics that prior bubbles lacked, including profitable cash-generating leaders and massive physical infrastructure investment. Whether the cycle ends in a 1999-style crash or a more orderly multi-year consolidation will depend on how earnings evolve relative to expectations over the next twelve to twenty-four months.

Jones himself is not selling — he is adding to AI positions while warning about the eventual exit. The rational response for most investors is not to exit but to ensure their AI exposure is appropriately sized, diversified, and complemented by hedges or non-correlated assets. Selling everything at the first warning is how investors miss the final, often largest, leg of bull markets.

The ratio compares the total value of publicly traded equities to the size of the underlying economy. Historically, ratios above 100% have indicated rich valuations and ratios above 150% have preceded notable corrections. A ratio of 300%–350% would imply that equity prices reflect roughly three times the annual output of the U.S. economy, a level that has no historical precedent and that would require either extraordinary earnings growth or a major reset to bring back into normal range.

The most important structural differences are real earnings, real infrastructure, and a much larger addressable market. Today's leading AI companies are reporting tens of billions of dollars in actual quarterly revenue, building physical data center and grid capacity that has lasting value, and addressing markets that include knowledge labor across the entire economy rather than just IT spending. None of this guarantees that valuations cannot correct severely, but it does suggest that the long-term productivity story is more robust than what underlay the 1999 rally.

The most effective protections are structural rather than tactical: appropriate position sizing, asset class diversification beyond U.S. tech, allocations to defensive sectors and gold, and selective use of options-based hedges for the portion of the portfolio where you are unwilling to accept full drawdown risk. Trying to perfectly time the top is far less reliable than building a portfolio that survives the top no matter when it comes. Reviewing strategies to invest in financial markets the right way is a useful starting point.

Jones described the cycle as roughly 50%–60% complete and suggested another year or two of upside before the eventual peak. Notably, prediction market data referenced in some recent reporting has placed the implied probability of an AI-driven market crack-up by the end of 2026 at only around 21%, broadly consistent with Jones's view that the cycle still has runway. Of course, prediction markets are sentiment indicators, not forecasts, and the timing of major regime shifts is notoriously hard to pin down.

Diversified AI ETFs carry less single-name risk than concentrated stock positions, which is genuinely valuable in late-cycle environments where any individual leader could underperform sharply. They are not, however, immune to systemic AI-sector drawdowns, since their constituents are often correlated. ETFs are a tool for managing single-name risk, not for eliminating sector risk.

The answer depends on personal risk tolerance, time horizon, and existing portfolio composition. A useful framework is to size AI exposure such that a 50% drawdown in that segment would be uncomfortable but not catastrophic for your long-term goals, then complement it with allocations to international equities, fixed income, defensive sectors, and tangible assets. Tools like technical and fundamental analysis can help refine entry and exit decisions within each segment.

The most useful framing of Paul Tudor Jones's warning is not "the AI bull market is a bubble" but rather "the AI bull market is a real productivity cycle that is now entering its more dangerous phase." Both halves of that sentence matter. Investors who only hear the first half will exit too early and miss substantial returns. Investors who only hear the second half will stay too long and surrender those returns in a brutal mean reversion.

The right posture for 2026 is one of strategic optimism: stay invested in the productivity revolution, but engineer your portfolio so that you can survive a 1999-scale correction if and when it arrives. That means appropriate position sizing, real diversification, deliberate use of hedges, and — most importantly — the behavioral discipline to follow your own rules when sentiment is screaming the loudest.

History is not a script. The 1999 parallel could play out within months, drag on for years, or never fully materialize because the underlying earnings story turns out to be stronger than the skeptics expect. What history reliably teaches, however, is that the investors who navigate full cycles successfully are not the ones who predict the future best. They are the ones who build portfolios robust enough that the future does not need to be predicted in order to compound wealth steadily.

If you are ready to bring institutional-grade structure to your investment approach — combining AI-driven analysis, disciplined risk management, and a long-term portfolio framework — explore how AssetWhisper can transform your investment portfolio and discover the systems we use to position for both upside and resilience in markets exactly like this one.

Related Reading on AssetWhisper: